Sarah is 36, a secondary school teacher in Melbourne. She has a $620,000 variable-rate mortgage she took out in 2023. Last year she got some relief — the RBA cut three times, dropping the cash rate to 3.60%. Her monthly repayment fell by about $170. Today that relief is gone. The RBA has now hiked three times in 2026, taking the cash rate to 4.35% — its highest level since late 2011. Sarah is paying approximately $280 more per month than she was at last year's low. Annualised, that is $3,360 she does not have.

More than 95% of Australian mortgages are variable rate. According to Roy Morgan Research, 1,447,000 Australians — 26.8% of all mortgage holders — were already at risk of mortgage stress in March 2026, before today's hike. Their projection: that figure rises to 1,604,000 Australians (30.3%) after today's decision. That would be an 18-year high, above the levels seen during the Global Financial Crisis.

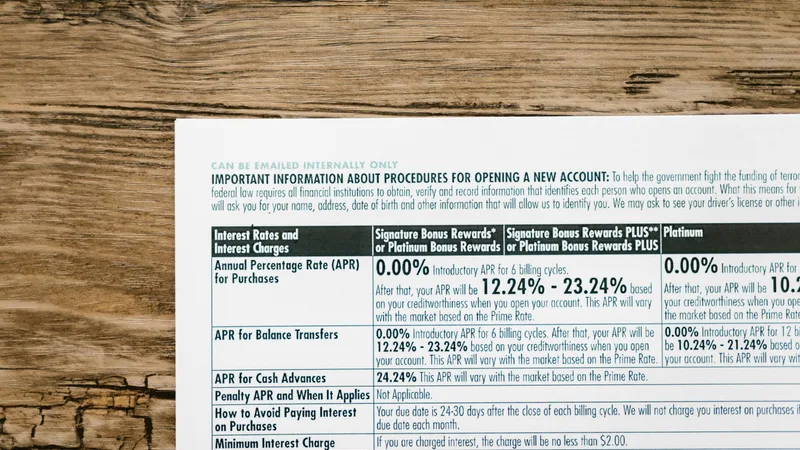

Australia Interest Rate Forecast 2026–2028 (RBA + Big 4)

The current Australian cash rate is 4.35% (set 5 May 2026 — its highest level since 2011). Major-bank forecasts now disagree on what comes next. Here is the consolidated RBA forecast view from Westpac, CBA, NAB, ANZ, and the RBA's own Statement on Monetary Policy:

| Period | Cash-rate forecast (consensus) | Likely next move |

|---|---|---|

| Q3 2026 | 4.35% (hold) | Hold-for-longer; ANZ flags ~25% chance of +25bps |

| Q4 2026 | 4.10% – 4.35% | First cut window opens late 2026 if CPI continues easing |

| End 2027 | 3.50% – 3.85% | 2–3 cuts through 2027 as neutral rate stabilises |

| End 2028 | 3.10% – 3.60% | Neutral-rate plateau; further easing depends on labour market |

Sources: RBA Statement on Monetary Policy (May 2026); Westpac, CBA, NAB, ANZ rate-call updates (May–June 2026). Forecasts are bank-consensus midpoints, not guarantees. The RBA explicitly avoids forward guidance.

When will Australian interest rates drop?

The earliest plausible cut is December 2026, with most Big 4 forecasters now centred on Q1–Q2 2027 for the first 25bps reduction. Cuts depend on three signals: (1) trimmed-mean CPI consistently below 3% (currently 3.2%), (2) unemployment drifting above 4.5%, and (3) wage growth easing under 3.5%. None of those triggers have fired yet, which is why none of the Big 4 are calling rate cuts before September 2026. If the next CPI print surprises lower, expectations will pull forward — if it surprises higher, ANZ's +25bps scenario gains weight.

Are interest rates likely to go up again in Australia? The base case across Big 4 forecasts is "no" — the May 2026 hike is most commonly called as the peak. ANZ is the lone outlier, assigning ~25% probability to one more hike before the cycle turns. Westpac and CBA both forecast hold-then-cut. The honest read for borrowers: don't position your finances on the assumption of cuts, but don't double down on further hikes either. Build the buffer that survives both scenarios — see the next-rate-move repayment table below for exact dollar impact at your loan size, or model your own scenario with the Velofy loan calculator which includes a ±25bps toggle.

The Cumulative Damage — Three Hikes in 2026

The story of Australian mortgage holders in 2026 is a story of relief given and taken away. After cutting the cash rate three times during 2025 to a trough of 3.60%, the RBA reversed course in February 2026 — citing persistent inflation and a strong labour market. Each hike was 25 basis points. Today's decision is the third of the year.

| Date | Decision | Cash Rate | Change vs Trough (3.60%) | Extra Monthly Cost ($600K loan) |

|---|---|---|---|---|

| Aug–Dec 2025 | 3 cuts (easing cycle) | 3.60% | — Trough | — |

| 4 Feb 2026 | +25bp hike | 3.85% | +0.25% | ~$91/month more |

| 18 Mar 2026 | +25bp hike | 4.10% | +0.50% | ~$182/month more |

| 5 May 2026 | +25bp hike | 4.35% | +0.75% | ~$273/month more |

Monthly repayment estimates for a $600,000 P&I variable loan, 30-year term, using standard RBA formula. Actual repayment depends on your lender's standard variable rate (SVR). The cumulative 75bp from the trough adds approximately $335/month to the average new loan size of $736,257 (April 2026, money.com.au). Source: Canstar, RBA.

"1,604,000 Australians — 30.3% of all mortgage holders — projected at risk of mortgage stress after today's hike. An 18-year high."— Roy Morgan Research, March 2026 projection (mr-10198)

Who Is Most at Risk?

Roy Morgan Research identifies mortgage holders as "at risk" when their mortgage repayments exceed a defined share of household income. As of March 2026 — before today's decision — 1,447,000 Australians (26.8%) were already in this category, with 1,020,000 (18.9%) classified as "extremely at risk."

The households most exposed are those who took out large loans in 2021–2023 during the ultra-low rate period, when the cash rate was as low as 0.10%. These borrowers were assessed at a stressed rate of at least 5.25% (the APRA buffer floor), but the speed of the subsequent hiking cycle — and now this 2026 reversal — has compressed their financial buffers faster than expected. First home buyers in Sydney and Melbourne with loan-to-value ratios above 80% are disproportionately represented — Brisbane buyers are relatively insulated thanks to QLD's $0 stamp duty on new homes for FHBs at any price (model the saving with the QLD stamp duty calculator).

How Much Does the Hike Actually Cost You?

The monthly impact depends on your loan balance and remaining term. Each 25bp increase on a 30-year P&I loan adds approximately $16 per $100,000 of outstanding principal.

| Loan Balance | +25bp (today's hike) | +75bp cumulative (since 3.60%) | Annualised extra cost |

|---|---|---|---|

| $400,000 | +~$60/month | +~$182/month | ~$2,184/year |

| $600,000 | +~$91/month | +~$273/month | ~$3,276/year |

| $736,257 (avg new loan) | +~$112/month | +~$335/month | ~$4,020/year |

| $900,000 | +~$136/month | +~$409/month | ~$4,908/year |

Enter your loan balance, current rate, and term — Velofy models P&I vs interest-only, offset impact, and which lenders are currently offering below-market rates.

Model My Mortgage → Free · ASIC-compliant · No signup

What the Next Rate Move Means for Your Repayments

The May 2026 hike to 4.35% may or may not be the cycle peak. Major-bank forecasts disagree on what comes next. Here is what each plausible next move does to a $750,000 P&I mortgage at the current 6.85% variable rate over a 30-year term — using the same APRA +3% buffer logic that lenders apply to your serviceability.

| Next RBA move | New variable rate | Monthly repayment | Change vs today |

|---|---|---|---|

| +25bps hike (4.60%) | 7.10% | $5,036 | +$125/mo |

| Hold (4.35%) | 6.85% | $4,911 | $0 (baseline) |

| −25bps cut (4.10%) | 6.60% | $4,786 | −$125/mo |

| −75bps cuts to 3.60% (full reversal) | 6.10% | $4,541 | −$370/mo |

Where the major banks sit on the next move: Westpac and CBA both forecast the May 2026 hike as the peak, with the first cut arriving late 2026 or early 2027. ANZ flags a 25% probability of one more hike before the cycle turns. NAB now sits on hold-for-longer. None of the Big 4 are forecasting cuts before September 2026.

The honest read: a single 25bps cut saves $125/month on $750k — meaningful but not life-changing. The bigger lever you can pull right now is rate negotiation with your lender (most variable borrowers are eligible for a 0.20-0.50% discount on request) or refinancing if your current rate sits above 6.85%. Don't wait for the RBA when you can move yourself.

The Velofy loan calculator includes a "what if rates change" toggle. Adjust by ±25bps to see your exact monthly change at your loan size.

Open Loan Calculator5 Ways to Reduce Your Mortgage Costs Right Now

Each of these actions is available today — no new loan required for the first three.

- Call your lender and ask for a rate reduction. This is the fastest move and costs nothing. Lenders know retention is cheaper than acquisition. In a competitive market, many banks have offered 10–30bp loyalty discounts to borrowers who call and threaten to refinance. Be specific: "I'm looking at [competitor rate] — what can you do?" Reference the RBA hike and the current market rate environment.

- Refinance to a challenger lender. The difference between a major bank standard variable rate (SVR) and the sharpest challenger lender offers is typically 0.5–1.0% per annum. On a $600K loan, 0.5% saves approximately $180/month — more than the cost of today's hike. Refinancing costs (discharge fee, application fee, valuation) typically total $1,000–$2,000 and pay back in months at these margins. According to Canstar (May 2026), cashback refinance offers from select lenders range from $2,000 to $10,000 in addition to a lower rate.

- Direct every spare dollar into your offset account. An offset account reduces the principal on which interest is charged — dollar for dollar. If you have $30,000 sitting in a transaction account earning minimal interest, move it to offset. At 4.35%, $30K in offset saves approximately $108/month. This is an immediate, zero-cost return of 4.35% p.a. — better than most savings accounts.

- Switch to weekly or fortnightly repayments. If you currently pay monthly, switching to fortnightly repayments at exactly half your monthly amount results in 26 payments per year (equivalent to 13 monthly payments). This reduces principal faster and cuts total interest over the life of the loan — typically by 2–4 years on a 30-year mortgage with no change to your actual weekly cash flow.

- Review your interest-only period if you have one. Investors on interest-only loans are assessed on the equivalent P&I repayment rate for serviceability, but are actually paying less each month. As rates rise, the gap between IO and P&I widens. If your IO period is expiring, get ahead of it — the transition to P&I at 4.35% will be a large step-up. Discuss refinancing options with a broker before the IO period ends.

- RBA cash rate hiked to 4.35% on 5 May 2026 — highest since late 2011

- Three 2025 rate cuts now fully reversed — plus 25bp more

- Cumulative cost (vs 3.60% trough): ~$273/month on a $600K loan

- Projected 1,604,000 Australians at mortgage risk — an 18-year high (Roy Morgan)

- More than 95% of Australian mortgages are variable rate and directly affected

- Fastest action: call your lender today and request a rate reduction — many will offer 10–30bp before you refinance

Velofy shows current lender rates and models your exact saving from refinancing — including cashback offers available now.

Compare Lenders → Free · ASIC-compliant · No signupCovers exactly what to do when rates rise: which bucket to draw on, how to negotiate a rate reduction with your bank, and when refinancing makes financial sense.

Shop on Amazon AU →Track your offset balance, extra repayments, and monthly cash position — helps you find the spare dollars to put against your loan when rates are rising.

Shop on Amazon AU →Frequently Asked Questions

What is the RBA cash rate in May 2026?

The RBA raised the cash rate to 4.35% on 5 May 2026 — its third hike of 2026 and the highest rate since late 2011. The prior rate was 4.10% (effective 18 March 2026). The cumulative increase from the 2025 trough of 3.60% is 75 basis points. Source: RBA (rba.gov.au).

How much does the May 2026 hike add to a $600K mortgage?

Today's 25bp hike adds approximately $91/month to a $600,000 P&I variable-rate mortgage on a 30-year term. Cumulatively, the three 2026 hikes add approximately $273/month compared to the 3.60% trough. On the average new loan of $736,257 (April 2026), the cumulative impact is approximately $335/month. Source: Canstar, RBA.

How many Australians are in mortgage stress after the May hike?

Roy Morgan projected approximately 1,604,000 Australians (30.3% of mortgage holders) at risk of mortgage stress if a May hike proceeded — an 18-year high. In March 2026 (before the hike), 1,447,000 (26.8%) were already at risk. Source: Roy Morgan Research (mr-10198, March 2026).

Will the major banks pass on the full 0.25% rate hike?

CBA, ANZ, NAB, and Westpac passed on the full 25bp from both the February and March 2026 RBA hikes within 2–5 business days. The same is expected for May. Check your lender's announcement for the exact effective date on your loan.

What can I do to reduce my repayments after the May hike?

Five options: (1) Call your lender and negotiate a loyalty rate reduction — many offer 10–30bp without formal refinancing. (2) Refinance to a challenger lender — typical savings of 0.5–1.0% p.a. on a $600K loan = $180–360/month. (3) Maximise your offset account — $30K in offset saves ~$108/month at 4.35%. (4) Switch to fortnightly repayments to reduce principal faster at no extra cost. (5) Review your interest-only period before it expires — plan the transition to P&I now. Source: ASIC MoneySmart.

Sources

- RBA — Cash Rate Target (rba.gov.au)

- Roy Morgan Research — Mortgage Stress Risk March 2026 (mr-10198)

- Canstar — What to Expect from the RBA in May 2026

- money.com.au — Average Mortgage Australia: Home Loan Statistics 2026

- ASIC MoneySmart — Mortgage Stress and What to Do

- savings.com.au — How the Big Four Banks Responded to the March 2026 RBA Hike